If you could get just ONE thing only for you & your baby, make it health insurance.

American ranks #1 in terms of highest cost of giving birth, so any coverage you can get to offset that hefty bill will lift a huge burden off your shoulders.

Without insurance, your hospital bill alone will blow all the other costs of having a baby out of the water.

Whether or not you can get health insurance in place before your wee one’s grand entrance, it’s still smart to learn what to anticipate with your future hospital bill.

That way, you can take advantage of ways to cut down the portion you pay out of pocket (which you’re likely to have, even if you do have insurance).

I’ll show you my labor and delivery bill breakdown, so you can see the actual numbers of my hospital birth cost.

Disclosure: Opinions expressed are our own. If you buy something through any of our affiliate links on this page, we may earn a commission at no extra cost to you. Thanks for supporting our site.

A few disclaimers

Note: Every circumstance is different, so your costs may vary.

These figures are based on my personal experience only, and are intended to help first-time parents navigate the finances of having a child with at least some frame of reference rather than going in totally blind.

Be aware that you may spend less or more, depending on your individual situation.

As helpful as I will try to be in this article, hospitals, healthcare, and Mother Nature don’t make it easy to give you a solid estimate.

From hospital to hospital, prices range widely even if it’s for a similar type of birth. For example, an uncomplicated vaginal delivery can be a few thousand to over $30,000.

Insurance coverage is also vastly different, depending on the details of your particular plan and also your insurance company’s interpretations of what is to be covered by law.

And Mother Nature is the most finicky of all. No matter how healthy and prepared you try to be to give yourself the best chance at having a normal, uncomplicated birth, stuff comes up.

And when those unexpected turns happen, more medical care means more charges on your hospital bill.

How to find out your estimated out-of-pocket costs

The closest you can get to finding out what you can expect to pay is to pick up the phone and call both your medical provider and insurance company to ask.

Fair warning: they’ll probably tell you “every situation is different so we can’t provide details on the numbers” and then quote you a figure in the thousands that you’ll just have to accept.

And even then, that number definitely won’t be exact if you throw other factors into the mix (i.e. complications during birth).

But knowing this now and having time to start saving or preparing is much better than getting thrown for a loop when you receive a jaw-dropping bill in the mail.

My health insurance coverage situation

Knowing my health insurance coverage will give you some context for understanding the breakdown of my particular bill:

- Location: Honolulu, Hawaii

- Health plan: A standard plan, where I had to cover 15% of the bill out-of-pocket

- When I gave birth to my son: February 2017

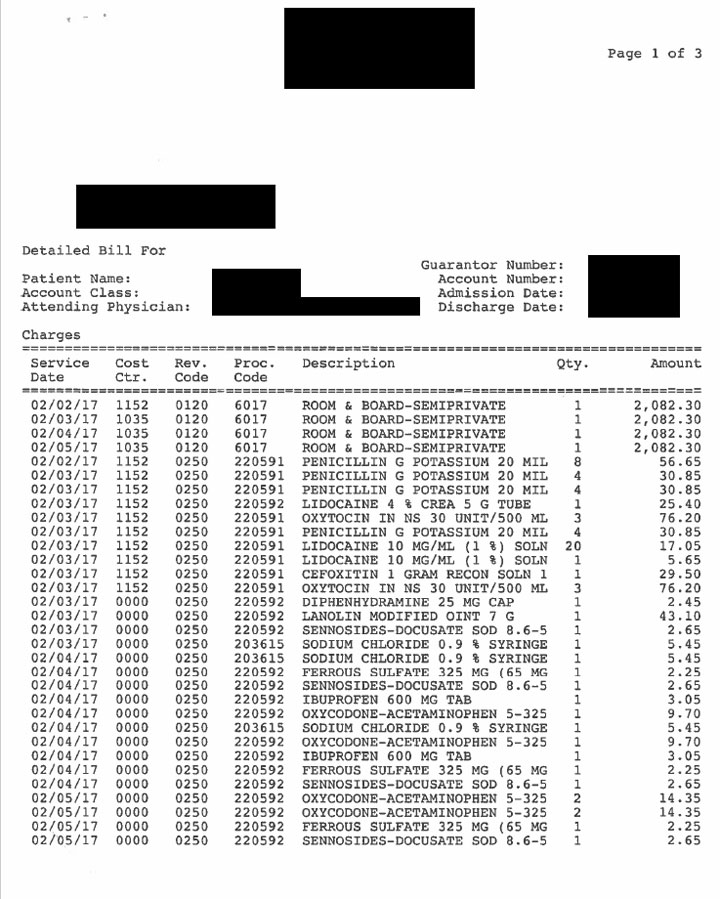

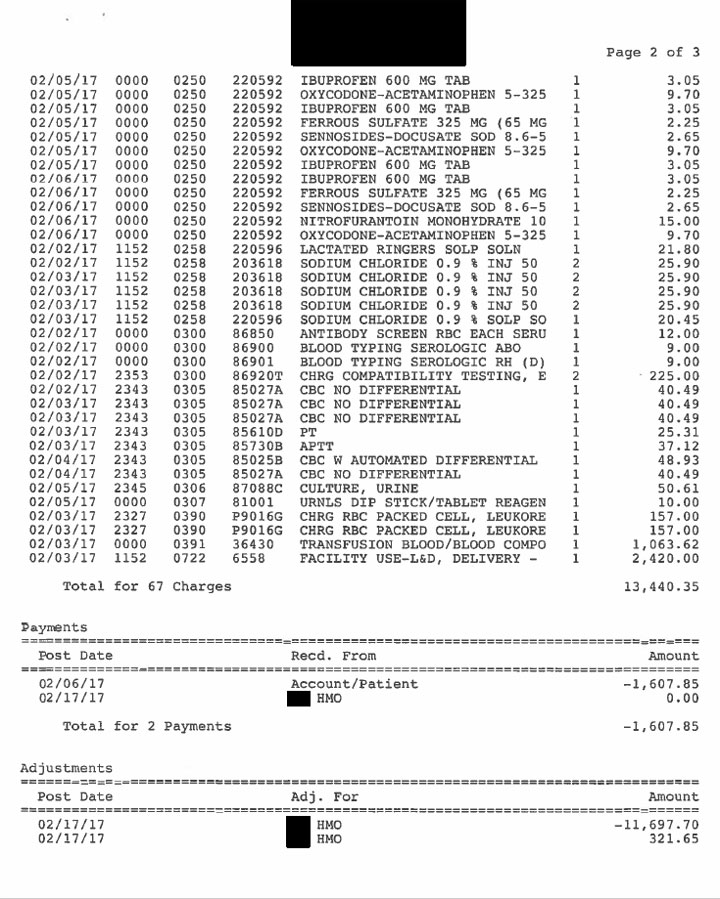

Labor and delivery bill breakdown

The table below shows an overview of the itemized hospital bill for my labor and delivery expenses that I was charged for.

Underneath that is detailed commentary on things I wanted to point out, including which items are not usual costs due to my having a complicated delivery.

| Item | Total Price |

| HOSPITAL STAY | |

| Room and board, semiprivate (4 nights) | $8329.20 |

| Facility for labor and delivery | $2420.00 |

| DRUGS & PILLS | |

| Penicillin | $149.20 |

| Lidocaine | $48.10 |

| Oxytocin | $152.50 |

| Cefoxitin | $29.50 |

| Diphenhydramine | $2.45 |

| Sennosides-docusate sodium | $15.90 |

| Sodium chlorate | $140.40 |

| Ferrous sulfate, a.k.a. iron (5 pills) | $11.25 |

| Ibuprofen (6 pills) | $18.30 |

| Oxycodone, a.k.a. extra, extra strength Tylenol (9 pills) | $77.20 |

| Lactated ringers | $21.80 |

| NURSING | |

| Lanolin (single use) | $43.10 |

| ADDITIONAL CHARGES FOR COMPLICATIONS | |

| Urine sample and test strip | $60.61 |

| Nitrofurantoin monohydrate | $15.00 |

| Blood transfusion | $1063.62 |

| Other blood stuff | $842.41 |

| TOTAL (before insurance) | $13,440.35 |

| Total covered by insurance |

$11,376.05* |

| TOTAL (out-of-pocket) | $2064.30 |

Room and board: I was admitted at 9:00pm on the first night, which means I got charged a full day’s rate for only 3 hours. I also had to stay an extra day for additional monitoring due to my complications.

Most people stay 2 days for uncomplicated pregnancies, or 3 days for cesarean sections (c-sections).

Penicillin: I tested positive for a weird strain of strep that is sometimes found in the vaginal canal and can be potentially harmful to the baby. I needed penicillin to keep it at bay so it wouldn’t transfer to baby during delivery.

Lidocaine: I didn’t get an epidural (and yes, childbirth is 100% as painful as they make it out in the movies), but I did get this pain-numbing medicine when they had to intervene with forceps to get the baby out.

You probably won’t see this charge, but if you opt for an epidural, then that would be added to your bill.

Oxytocin: Since my baby was not coming out in a timely manner, this hormone was administered to induce labor.

Cefoxitin: Some type of antibiotic that stops growth of bacteria, presumably working in conjunction with the penicillin because of that strep thing? Not sure of the exact purpose but I apparently paid for it.

Diphenhydramine: Antihistamine; not sure what this was for.

Sennosides-docusate sodium: Laxative and stool softener. I suppose because mothers are kinda broken downstairs afterwards, this helps to alleviate the hardness of the #2.

Lactated ringers: A mixture of water and electrolytes administered via IV.

Iron pills, ibuprofen, prescription tylenol: Dang this stuff is expensive when you get them from the hospital.

For reference, the cost of 5 iron pills was double what I paid for a bottle of 100+ tablets*, which I actually bought with me to the hospital as part of my prenatal vitamins.

When I asked if I could take my own iron pills, the hospital staff said it could interfere with the other medications they were administering so it wasn't advised. Argh.

Update: When I gave birth to my second son, I brought my own iron pills and the doctor said it was fine.

Lanolin: This one irks me real bad. It’s nipple cream that costs $7 for a full bottle, outside of the hospital. This $43.10 is for a one-time sample size.

I told them I didn’t want it because I had my own organic nipple cream*, but the nurse said she already scanned it so I had to take it.

That I had to pay $43.10 for something I expressly declined is ABSURD.

Urine sample and test strip: After giving birth, I could not for the life of me get my body to pee on its own for 3 days. Fun times. I had a catheter stuck in me, but I guess not being able to flush your urine out makes you more prone to UTI. Ugh.

Nitrofurantoin monohydrate: To treat abovementioned UTI.

Blood transfusion and other blood stuff: I lost enough blood during the delivery process that I needed a blood transfusion.

Because they have to be extra careful that the blood being given is compatible with your body so you don’t die, they have to do a lot of precautionary things that drive up this cost.

*Insurance coverage: if you look towards the bottom of the bill, you will see a section with HMO coverage. They covered $11,697.70, but added $321.65 back to my bill, so the total that was covered is $11,376.05

My actual hospital bill

Here are scans of my hospital birth costs for your perusal:

The third page of my bill basically said the following:

Total for 2 adjustments: -$11,376.05

Pay this amount: $456.45

Total labor and delivery bill

If I had no insurance coverage, I would have had to pay a whopping $13,440.35 out of pocket.

Luckily, I did, so insurance covered $11,697.70, but they readjusted an additional $321.65 to my bill, so I ended up paying $2064.30 out of pocket.

As if that isn't enough, the labor and delivery bill is not the only bill you’ll get.

Patients are often billed separately for things like the delivery doctor, the pediatrician, ambulance or emergency room services, and pharmacy charges for any medications you take home.

Taking all the medical costs I incurred related to the delivery and hospital stay into account, my total out-of-pocket expense was $2,553.15. This included:

- the doctor for my delivery

- the doctor for baby’s delivery (which I’m pretty sure was the same doctor for the same thing, but they just split the bill between myself & my son)

- extra meds

How to choose health insurance coverage for mom and baby

Now that you have an idea of what the numbers might look like, here are some tips about how to pick your coverage.

Of course, what kind of services or doctors you want may be important factors to you, but speaking strictly from a financial standpoint, there are 3 considerations that will help you when determine which insurance plan to go with:

1) Insurance premium costs

If you have the opportunity to switch carriers before your child is born, take the time to compare the different plans offered through your and your partner’s employer.

See how much will be deducted from your paycheck. Consider what the total premiums will be for the entire duration you are under the plan (usually one year).

2) Out-of-pocket expenses

What you are expected to pay out of pocket depends on the plan you choose. Here are some key terms to pay attention to:

- Deductible: the amount you must pay first before any insurance coverage kicks in

- Copay: a flat amount or percentage you must pay each time a particular service is rendered

- Out-of-pocket limit: The max you can be billed in the policy period for all your services

When reviewing what services are covered, pay attention to these ones that are specifically related to giving birth:

- Hospital stay/facility services: how much you are expected to cover for use of a hospital or clinic

- Physician/OB-GYN/specialist services: how much you are expected to cover for the people and things that involve your downstairs and getting a baby out of it

TIP: Ask your (or your partner’s) employer for a copy of the benefits handbook before calling.

The handbook will outline is covered under the insurance plan offered by your workplace, and usually has a chart that shows you the dollar amounts and percentages you will be charged out-of-pocket.

3) Clarification from your health insurance carrier

Insurance-related stuff and figuring out what will be covered versus what will come out-of-pocket can get you feeling more nauseous than morning sickness.

Rather than try to figure it out on your own, pick up the phone and ask the health insurance carrier.

Here are some specific questions you may want to ask regarding your coverage:

- What labor and delivery benefits are covered in my plan? (ask for different scenarios, from an uncomplicated vaginal delivery to emergency c-section)

- What common labor and delivery costs are not covered by my plan?

- Which hospitals are in my insurance’s network?

- How long of a hospital stay is covered after delivery? What kind of room arrangement is covered (private, shared)?

- (If this is your thing) Do you cover any nontraditional deliveries (home birth, etc)?

- How do I make sure my baby gets health insurance coverage from the moment of delivery?

Here are some other scenarios that will drive up the hospital cost, which you should inquire about as well:

- Getting induced

- Needing a c-section

- Having some other method of intervention (eg: forceps)

- Doulas

- Having an untraditional birth

TIP: Keep good records of who you talk to regarding your plan coverage and bills. Mark who you spoke to, the ID number or extension of the representative, and the date you spoke to them.

Example plan comparison

When you are armed with all this information, you can do a comparison of the overall costs in different scenarios to see which plan you want to go with.

Here’s a sample walkthrough of how I compared the two plans offered by my employer:

| Plan 1 | Plan 2 | |

| Coverage | 100% covered by insurance; no deductible, copay or coinsurance |

85% covered by insurance; 15% out-of-pocket |

| Premium cost | $407.03 per paycheck, or $814.06 per month (2 paychecks a month) |

$99.22 per paycheck, or $198.44 per month (2 paychecks a month) |

| Premium for full enrollment period (one year) | $9768.72 ($814.06 x 12 months) |

$2381.28 ($198.44 x 12 months) |

| Out-of-pocket costs | $0 | $1800 (estimate from insurance carrier for uncomplicated delivery) $3600 (estimate from insurance carrier for c-section) |

| Total amount I am paying | $9768.72 | $4181.28 for regular birth ($2381.28 for premiums + $1800 billed to me out of pocket) $5981.28 for c-section ($2381.28 for premiums + $3600 billed to me out of pocket) |

Under this example, I stood to save about several thousand dollars by going with Plan 2, so that’s what I did.

This assumes there are no other considerations that would change your decision, such as choice of doctors, choice of hospital, etc.

TIP: This example doesn’t take into account any special tax benefits you might have, such as if you use a health flex-spending account or your premiums are paid with pre-tax dollars.

Remember to adjust your figures when calculating your estimated costs if the monies involved are being taxed differently under each plan.

Additional tips to save on the cost of giving birth

Tip 1. Get tax savings on health-related expenses.

Enroll in a health savings account or flex spending account if you qualify, both of which allow you to save on taxes for the expenses you pay out of pocket.

Tip 2. Understand your insurance plan’s benefits.

Know what is and isn’t covered, decide how important it is to get the things that aren’t covered, and know what things you can get without having to pay extra for it (like free baby supplies from the hospital!).

Tip 3. Make sure doctors and specialists are in your provider network.

Most insurance plans charge two different prices, depending on if your doctor or specialist is part of their preferred network. The price difference is pretty big, so be prepared if you are choosing a doctor from outside the network.

Tip 4. Try your best to stay healthy.

Virtually all services rendered will include copays, deductibles, and other costs. While you can’t guarantee there won’t be any complications, whatever you can do to keep them as few as possible will be better for you, the baby, and your wallet.

Conclusion

The cost of giving birth is one of the most important expenses to consider when planning for a baby.

By sharing my labor and delivery bill breakdown and health plan comparison, new parents who want to be financially prepared for the hospital birth cost will be better equipped to provide for the new addition to their family.

Read More

Brittni says

Hello, did you also have a separate bill for charges for you baby like newborn hospital care and such? Thanks!

Sylvia | Mommy Over Work says

Hi Brittni,

So there were multiple bills that came in that makes this confusing overall, but I believe the main one that is shown on this post is supposed to account for everything. The amount I had left to pay on the invoice I posted here, $456.45, matched an additional bill I received about a month later that I believe was to cover the expense of the doctor delivering the baby.

Sissi Chen says

Hi~thank you for your article! May I know how much you paid to your provider (your OB)? I am considering using an in-network hopstial bur an out-of-network OB. I am wondering how much on the bill form the OB since mine would be counted as out of network. Thank you!

Sylvia | Mommy Over Work says

Hi Sissi,

I tried looking for my bill but can't seem to find it. From what I remember, I think I paid something like $400 out of pocket. Sorry I'm not able to provide the total without insurance factored in. Hope all goes well for you!

Sylvia